Sara wanted money to fix her home kitchen. Her friend told her about a HELOC. Another friend suggested refinancing the home loan. Sara got confused because both options used home value. Many people face the same problem today.

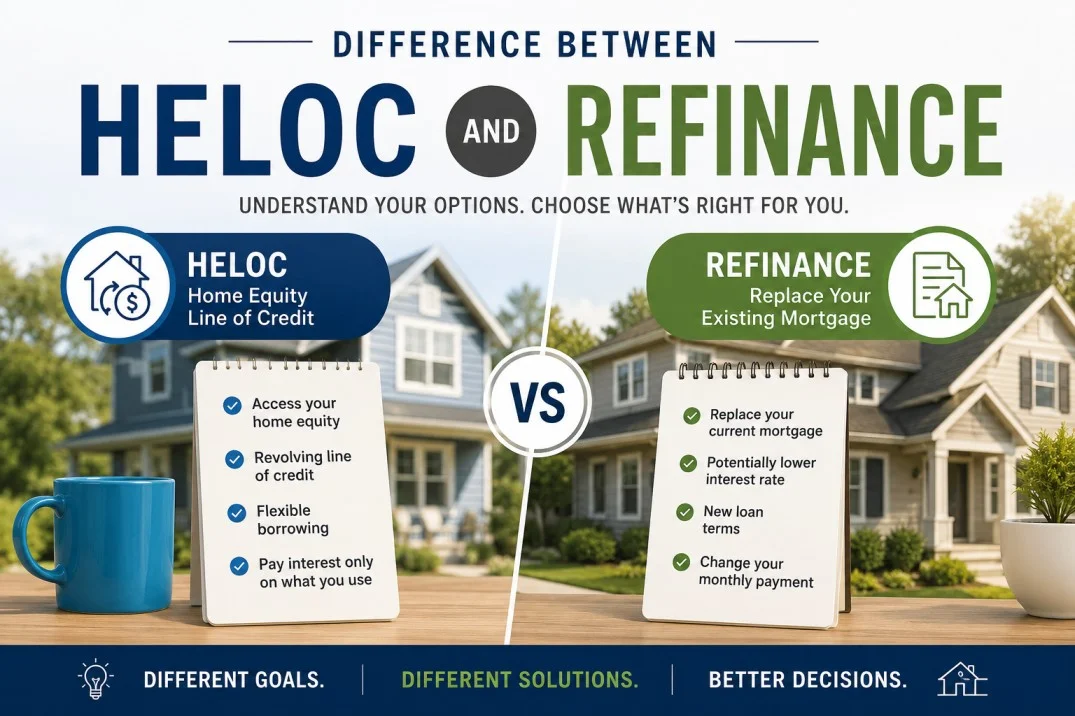

The difference between heloc and refinance is important when you want to borrow money using your house. Some people want lower monthly payments. Others need cash for repairs, school, or bills. That is why understanding the difference between heloc and refinance can help you make a smart choice.

Both options can help homeowners. However, they work in different ways. This guide explains everything in very simple words. You will also see examples, tables, and easy comparisons.

What is “HELOC”?

A HELOC means “Home Equity Line of Credit.” It lets homeowners borrow money from the value of their home. It works like a credit card. You can borrow money when needed and pay it back slowly.

Banks decide the limit based on your home equity. Home equity is the value of your home after subtracting the remaining loan balance.

History of HELOC

HELOC became popular in the United States during the 1980s. Banks wanted to give homeowners flexible borrowing options. Before that, people mostly used traditional loans. HELOC allowed people to borrow only the amount they needed instead of taking one large loan. Over time, homeowners started using HELOCs for home repairs, education costs, and emergencies. During housing booms, HELOC became very common because home values increased quickly. Today, many banks and lenders offer HELOC plans with different interest rates and repayment terms.

What is “Refinance”?

Refinance means replacing your old home loan with a new one. People refinance to get lower interest rates, reduce monthly payments, or change loan terms.

Some homeowners also use cash-out refinancing to get extra money from home equity.

History of Refinance

Mortgage refinancing became common in the 1930s after housing reforms in the United States. Governments and banks wanted to help families manage home loans better. Later, when interest rates dropped in different years, millions of homeowners refinanced their mortgages to save money. Refinance became even more popular in the early 2000s because lenders offered easier loan options. Today, refinancing is used worldwide. People refinance for lower payments, shorter loan terms, or extra cash for personal needs like education, medical bills, and home improvement.

HELOC vs Refinance

HELOC gives flexible borrowing from home equity. Refinance replaces your old mortgage with a new loan.

Both use your home’s value, but they work differently. Now let us explore them in detail.

How “HELOC” Works

A HELOC gives you a borrowing limit based on your home equity. You can take money little by little during the draw period.

Key Features

- Works like a credit line

- Borrow only what you need

- Usually has variable interest rates

- Uses home equity as security

- Flexible spending option

🔵 “I used a HELOC to pay for my daughter’s college fees.”

🔵 “Ali borrowed money from his HELOC to repair his roof.”

Uses

- Home repairs

- Medical bills

- Education expenses

- Emergency costs

- Small business needs

How “Refinance” Works

Refinancing replaces your current home loan with a new one. The new loan may have a lower rate or different repayment period.

Key Features

- Replaces old mortgage

- Can lower monthly payments

- Fixed or variable interest available

- May reduce loan years

- Cash-out option available

🟢 “Maria refinanced her loan to get a lower interest rate.”

🟢 “John used cash-out refinancing to renovate his house.”

Uses

- Lower monthly mortgage payments

- Change loan term

- Get lower interest rates

- Access extra cash

- Combine debts

Which One Should You Use?

Choose HELOC if you need flexible borrowing over time. It is good for ongoing expenses.

Choose refinance if you want a new mortgage with better terms or lower monthly payments.

10 Differences Between HELOC and Refinance

1. Loan Structure

HELOC

HELOC is a revolving credit line.

🔴 “She borrowed small amounts monthly.”

🔴 “The family used only part of the credit line.”

Refinance

Refinance replaces the full mortgage.

🔴 “They signed a completely new loan.”

🔴 “His old mortgage ended after refinancing.”

2. Interest Rates

HELOC

HELOC often has variable rates.

🔴 “The payment changed after interest rates increased.”

🔴 “Her HELOC became more expensive later.”

Refinance

Refinance may offer fixed rates.

🔴 “His monthly payment stayed the same.”

🔴 “They locked a lower fixed rate.”

3. Payment Style

HELOC

Payments depend on borrowed amount.

🔴 “She paid only for used money.”

🔴 “The balance changed every month.”

Refinance

Monthly mortgage payments stay regular.

🔴 “They paid the same amount monthly.”

🔴 “The new loan had fixed payments.”

4. Flexibility

HELOC

HELOC offers flexible withdrawals.

🔴 “He borrowed money when needed.”

🔴 “She used funds slowly over time.”

Refinance

Refinance gives one large loan.

🔴 “They received money once.”

🔴 “The loan amount stayed fixed.”

5. Loan Purpose

HELOC

Mostly used for ongoing expenses.

🔴 “The HELOC helped pay medical bills.”

🔴 “They used it during home renovation.”

Refinance

Often used for lowering mortgage costs.

🔴 “Refinancing reduced their payment.”

🔴 “The new rate saved money yearly.”

6. Closing Costs

HELOC

Usually lower closing costs.

🔴 “The bank charged small fees.”

🔴 “HELOC setup costs were cheaper.”

Refinance

Can have higher closing costs.

🔴 “They paid appraisal fees.”

🔴 “The refinance process cost more.”

7. Loan Term

HELOC

Has draw and repayment periods.

🔴 “He borrowed during the draw period.”

🔴 “Repayment started later.”

Refinance

Has a fixed mortgage term.

🔴 “Their loan lasted 15 years.”

🔴 “The mortgage ended after 30 years.”

8. Cash Access

HELOC

Money is available anytime during the draw period.

🔴 “She borrowed again after six months.”

🔴 “The credit line stayed open.”

Refinance

Cash comes one time in cash-out refinancing.

🔴 “They received a lump sum.”

🔴 “The bank paid them once.”

9. Risk Level

HELOC

Payments may rise with interest rates.

🔴 “His costs increased suddenly.”

🔴 “Variable rates made budgeting hard.”

Refinance

Fixed rates give stable payments.

🔴 “The payment stayed predictable.”

🔴 “They avoided interest surprises.”

10. Best For

HELOC

Best for flexible and repeated spending.

🔴 “The HELOC funded many projects.”

🔴 “She used it for yearly expenses.”

Refinance

Best for long-term mortgage savings.

🔴 “Refinancing reduced total loan costs.”

🔴 “They saved money every month.”

Why People Get Confused About Their Use

People get confused because both HELOC and refinance use home equity. Both also involve banks and mortgages. Many advertisements talk about “borrowing from your home,” which sounds similar. However, one is a credit line, while the other replaces your mortgage completely.

Table: Difference and Similarity

| Feature | HELOC | Refinance | Similarity |

| Loan Type | Credit line | New mortgage loan | Both use home equity |

| Payments | Flexible | Fixed or regular | Both require repayment |

| Interest Rate | Usually variable | Often fixed | Both charge interest |

| Cash Access | Borrow anytime | One-time amount | Both provide funds |

| Main Goal | Flexible spending | Better mortgage terms | Both help homeowners |

| Risk | Rates may rise | More stable | Both use home as security |

Which is Better in What Situation?

HELOC is better when you need money slowly over time. It works well for home repairs, education, or emergency expenses. It also gives flexible borrowing.

Refinance is better when you want lower mortgage payments or lower interest rates. It is also useful if you want a fresh loan with better terms.

How Are “HELOC” and “Refinance” Used in Metaphors and Similes?

🟣 “A HELOC is like a reusable wallet.”

🟣 “Refinance is like replacing old shoes with better ones.”

🟣 “HELOC flows like a tap of money.”

🟣 “Refinancing feels like resetting your financial journey.”

Connotative Meaning

HELOC

Usually seen as flexible but risky.

🟣 “The HELOC gave them financial freedom.”

🟣 “Too much HELOC debt created stress.”

Refinance

Usually seen as stable and smart.

🟣 “Refinancing helped them save money.”

🟣 “The refinance made budgeting easier.”

Idioms or Proverbs

🟣 “Don’t bite off more than you can chew.”

Meaning: Do not borrow more money than you can repay.

🟣 “A penny saved is a penny earned.”

Meaning: Saving money through refinancing is valuable.

Works in Literature

🟣 The Total Money Makeover — The Total Money Makeover by Dave Ramsey (2003)

🟣 Rich Dad Poor Dad — Rich Dad Poor Dad by Robert Kiyosaki (1997)

Movies Related to the Keywords

🟣 The Big Short — 2015, USA

🟣 99 Homes — 2014, USA

Frequently Asked Questions

1. Is HELOC the same as refinance?

No. HELOC is a credit line, while refinance replaces your mortgage.

2. Which option is cheaper?

It depends on interest rates, fees, and your financial needs.

3. Can I use HELOC for emergencies?

Yes. Many people use HELOC for emergency expenses.

4. Does refinancing lower monthly payments?

Yes. Refinancing may reduce payments if rates are lower.

5. Which option is more flexible?

HELOC is usually more flexible because you borrow when needed.

Final Words

Understanding HELOC and refinance can help you make smarter money decisions. Both options have benefits. The right choice depends on your needs, goals, and budget. Learn carefully before signing any loan papers.

Conclusion

The difference between heloc and refinance is simple once you understand their purpose. HELOC gives flexible access to money from home equity, while refinance replaces your current mortgage with a new loan. HELOC works well for ongoing expenses, but refinance is often better for lowering monthly payments or interest rates. Both can help homeowners manage money wisely. Before choosing either option, compare costs, risks, and long-term benefits carefully. A smart decision today can improve your financial future tomorrow.

Hi! I am Arshad Ullah presently working as linguist in Punjab Education Department. I have done MA in English Literature while M.Phil in Applied Linguistics. I have taught creative writing to the post graduation classes for 15 years. Presently I am working as content writer, and offering classes for blog writing.